Social Media

Nextdoor’s SPAC investor deck paints a picture of sizable scale and sticky users

The SPAC parade continues in this shortened week with news that community social network Nextdoor will go public via a blank-check company. The unicorn will merge with Khosla Ventures Acquisition Co. II, taking itself public and raising capital at the same time.

Per the former startup, the transaction with the Khosla-affiliated SPAC will generate gross proceeds of around $686 million, inclusive of a $270 million private investment in public equity, or PIPE, which is being funded by a collection of capital pools, some prior Nextdoor investors (including Tiger), Nextdoor CEO Sarah Friar and Khosla Ventures itself.

Notably, Khosla is not a listed investor in the company per Crunchbase or PitchBook, indicating that even SPACs formed by venture capital firms can hunt for deals outside their parent’s portfolio.

Per a Nextdoor release, the transaction will value the company at a “pro forma equity [valuation] of approximately $4.3 billion.” That’s a great price for the firm that was most recently valued at $2.17 billion in a late 2019-era Series H worth $170 million, per PitchBook data. Those funds were invested at a flat $2 billion pre-money valuation.

So, what will public investors get the chance to buy into at the new, higher price? To answer that we’ll have to turn to the company’s SPAC investor deck.

Our general observations are that while Nextdoor’s SPAC deck does have some regular annoyances, it offers a clear-eyed look at the company’s financial performance both in historical terms and in terms of what it might accomplish in the future. Our usual mockery of SPAC charts mostly doesn’t apply. Let’s begin.

Nextdoor’s SPAC pitch

We’ll proceed through the deck in its original slide order to better understand the company’s argument for its value today, as well as its future worth.

The company kicks off with a note that it has 27 million weekly active users (neighbors, in its own parlance), and claims users in around one in three U.S. households. The argument, then, is that Nextdoor has scale.

A few slides later, Nextdoor details its mission: “To cultivate a kinder world where everyone has a neighborhood they can rely on.” While accounts like @BestOfNextdoor might make this mission statement as coherent as ExxonMobil saying that its core purpose was, say, atmospheric carbon reduction, we have to take it seriously. The company wants to bring people together. It can’t control what they do from there, as we’ve all seen. But the fact that rude people on Nextdoor is a meme stems from the same scale that the company was just crowing about.

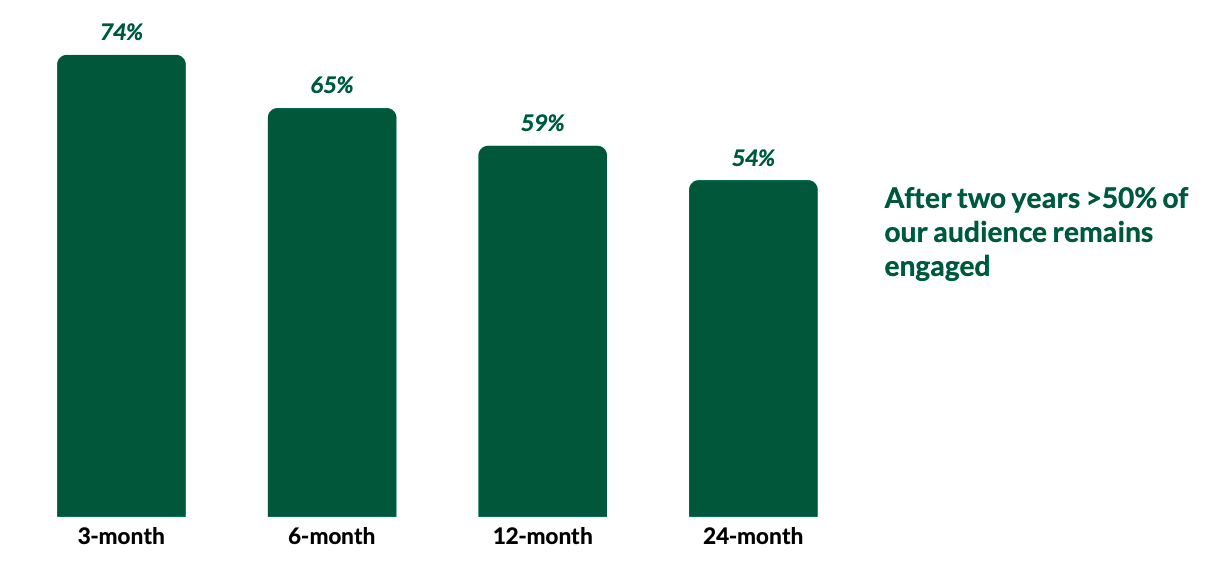

Underscoring its active user counts are Nextdoor’s retention figures. Here’s how it describes that metric:

Image Credits: Nextdoor SPAC investor deck

These are monthly active users, mind, not weekly active, the figure that the company cited up top. So, the metrics are looser here. And the company is counting users as active if they have “started a session or opened a content email over the trailing 30 days.” How conservative is that metric? We’ll leave that for you to decide.

The company’s argument for its value continues in the following slide, with Nextdoor noting that users become more active as more people use the service in a neighborhood. This feels obvious, though it is nice, we suppose, to see the company codify our expectations in data.

Nextdoor then argues that its user base is distinct from that of other social networks and that its users are about as active as those on Twitter, albeit less active than on the major U.S. social networks (Facebook, Snap, Instagram).

Why go through the exercise of sorting Nextdoor into a cabal of social networks? Well, here’s why:

Senate study proposes ‘at least’ $32B yearly for AI programs

‘Furiosa: A Mad Max Saga’ review: George Miller’s blazing action folktale might just have outdone ‘Fury Road’

Orange Charger thinks a $750 outlet will solve EV charging for apartment dwellers

Sex education is under threat in the UK. What’s going on?

Looking Glass launches new 3D displays

‘House of the Dragon’ Season 2 trailer breakdown: Dragons, Rook’s Rest, and more

AWS CEO Adam Selipsky steps down

The women getting guys to rate their nudes on Reddit

OpenAI Startup Fund raises additional $5M

Apple iPad Pro 2024 (13-inch) review: The battery life is bonkers

Former top SpaceX exec Tom Ochinero sets up new VC firm, filings reveal

Consumer Financial Protection Bureau fines BloomTech for false claims

Tesla layoffs hit high performers, some departments slashed, sources say

Langdock raises $3M with General Catalyst to help businesses avoid vendor lock-in with LLMs

This nova is on the verge of exploding. You could see it any day now.

India’s election overshadowed by the rise of online misinformation

What Robert Durst did: Everything to know ahead of ‘The Jinx: Part 2’

This camera trades pictures for AI poetry

Xaira, an AI drug discovery startup, launches with a massive $1B, says it’s ‘ready’ to start developing drugs

iPad Pro 2024 now has OLED: 5 reasons this is a big deal

Senate study proposes ‘at least’ $32B yearly for AI programs

‘Furiosa: A Mad Max Saga’ review: George Miller’s blazing action folktale might just have outdone ‘Fury Road’

Orange Charger thinks a $750 outlet will solve EV charging for apartment dwellers

Sex education is under threat in the UK. What’s going on?

Looking Glass launches new 3D displays

‘House of the Dragon’ Season 2 trailer breakdown: Dragons, Rook’s Rest, and more

AWS CEO Adam Selipsky steps down

The women getting guys to rate their nudes on Reddit

OpenAI Startup Fund raises additional $5M

Apple iPad Pro 2024 (13-inch) review: The battery life is bonkers

-

Business6 days ago

Business6 days agoAI chip startup DEEPX secures $80M Series C at a $529M valuation

-

Entertainment5 days ago

Entertainment5 days agoJinkx Monsoon promises ‘the queerest season of ‘Doctor Who’ you’ve ever seen!’

-

Business5 days ago

Business5 days agoStrictlyVC London welcomes Phoenix Court and WEX

-

Business7 days ago

Business7 days agoRetell AI lets businesses build ‘voice agents’ to answer phone calls

-

Entertainment5 days ago

Entertainment5 days agoHow to watch every ‘Law and Order’ online in 2024

-

Entertainment5 days ago

Entertainment5 days agoBookTok and teens: What parents need to know

-

Business4 days ago

Business4 days agoWhy Apple’s ‘Crush’ ad is so misguided

-

Entertainment6 days ago

Entertainment6 days ago'House of the Dragon' recap: Every death, ranked by gruesomeness