Startups

China’s secret startup advantage: liquidity

This year’s rush of IPOs from Chinese tech companies has dominated headlines, but what’s more interesting is how quickly they got there.

Traditionally, “going public” represented the gratifying culmination of sleepless nights and missed birthdays that went into building a company. The peak of a lengthy climb, where founders and VCs would finally see the fruits of their labor.

However, Chinese companies appear to be reaching that peak much quicker than their American peers, heading to the public markets only a few years after initial venture investments, and often with little operating history.

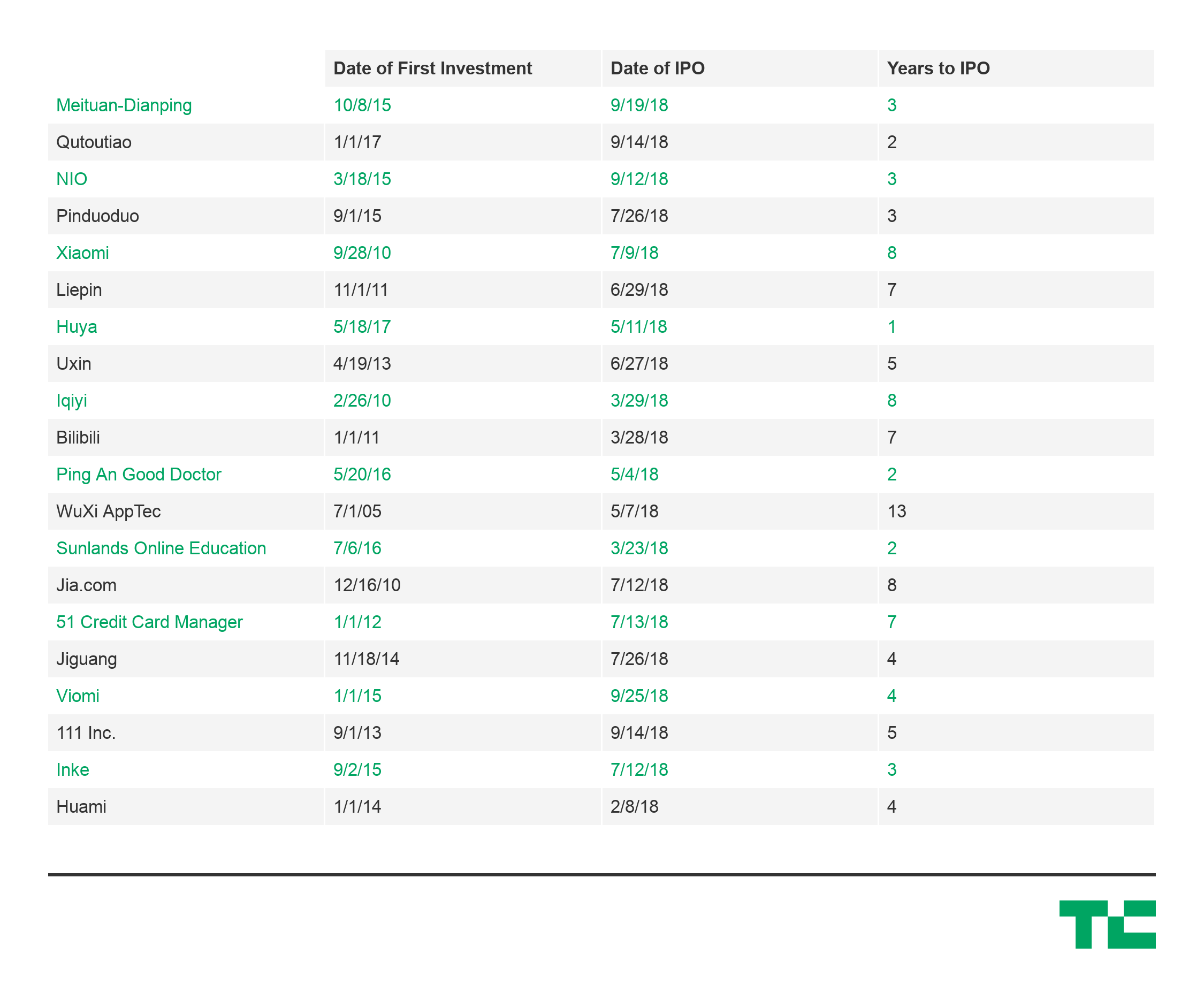

Analyzing twenty of the most high profile Chinese tech IPOs this year, the average time from first venture investment to IPO was only around three to five years. Take e-commerce platform Pinduoduo, which pulled in $1.6 billion less than three years after its Series A. Or the recent IPO of EV-manufacturer NIO, which raised a billion dollars just three-and-a-half years after its Series A and having just delivered its first car in June.

China IPO data for 2018 compiled from NASDAQ, Pitchbook, and Crunchbase

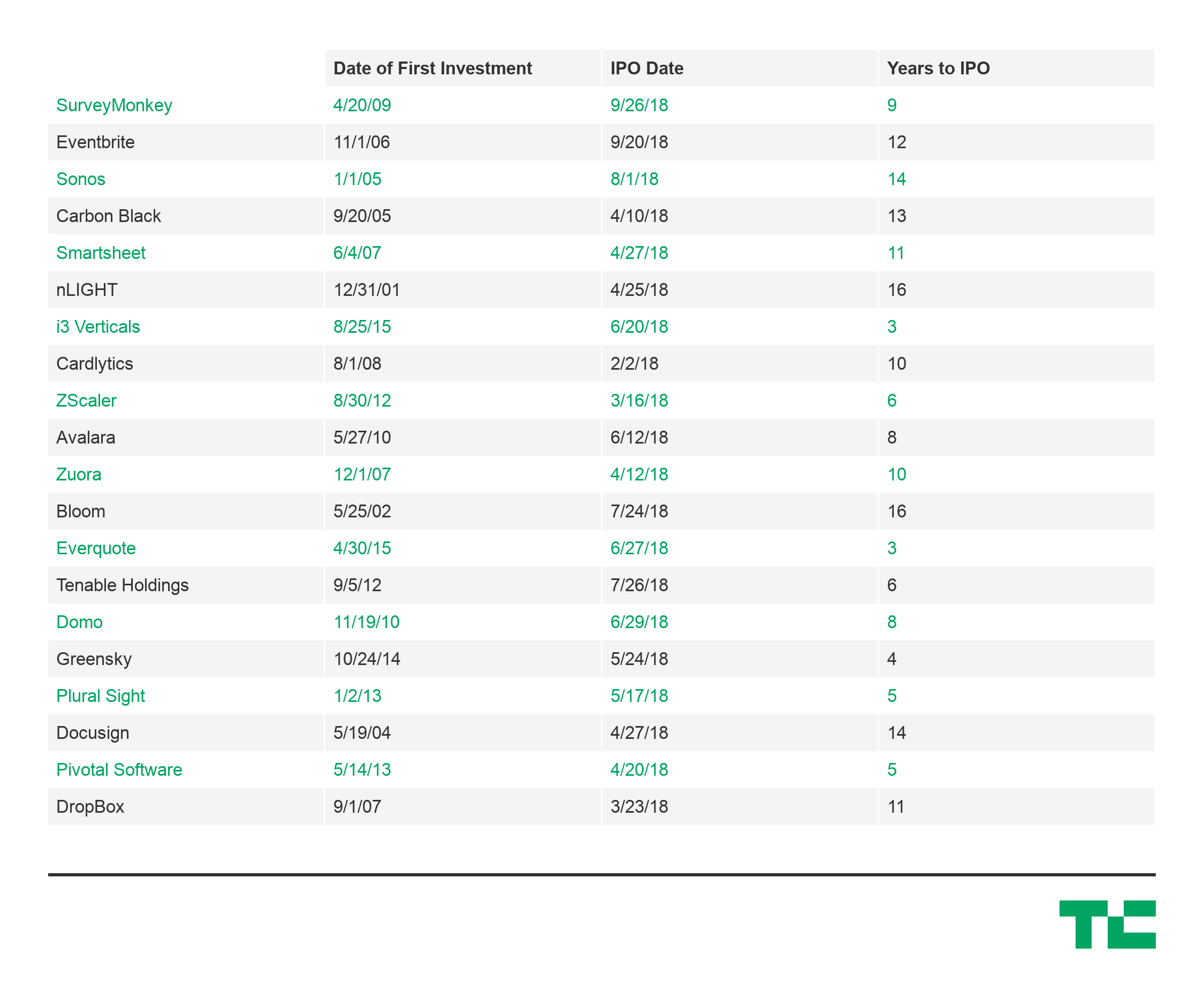

That’s less than half the average 10-year timeline for venture-backed US tech companies that went public in 2018, including Dropbox, Eventbrite, and DocuSign, which all IPO’d more than a decade after their initial investments.

Differences in market maturity, government involvement, and support from large tech incumbents all undoubtedly play a factor, but the speed to liquidity for the Chinese companies is still astounding.

Faster liquidity can push cycle of returns, fundraising, reinvestment

Speed to liquidity is a critical metric for the health of a startup ecosystem. It creates a positive cycle where faster liquidity can drive faster fundraising, faster reinvestment, faster startup building, and faster public liquidity again. An accelerated cycle could be especially appealing for funds with LPs that require faster returns due to cash commitments or otherwise.

It’s important to note that venture returns are a function of capital and time, so quicker exits will also drive higher returns for the same amount invested. For example, a $1 million investment with a $5 million exit after ten years would generate an Internal Rate of Return (a commonly used metric to evaluate VC performance) of 20%. If the same exit occurred after five years, the IRR would be 50%.

Liquidity is a key consideration as China’s influence on the flow of global venture capital intensifies. As China’s tech ecosystem sees more of its darlings mature and more consistently deliver smashing exits, investments in China will have to be a more serious consideration for VCs, even if only to minimize the sheer amount of time, resources, and painstaking energy needed to build a company in the U.S.

Thoma Bravo to take UK cybersecurity company Darktrace private in $5B deal

Summer Movie Preview: From ‘Alien’ and ‘Furiosa’ to ‘Deadpool and Wolverine’

Zomato’s quick commerce unit Blinkit eclipses core food business in value, says Goldman Sachs

Monsta X’s I.M on making music, gaming, and being called ‘zaddy’

Petlibro’s new smart refrigerated wet food feeder is what your cat deserves

The books on your favorite creators’ TBR shelf

Xaira, an AI drug discovery startup, launches with a massive $1B, says it’s ‘ready’ to start developing drugs

Rabbit R1 hands-on review: Something is iffy about this

UK probes Amazon and Microsoft over AI partnerships with Mistral, Anthropic, and Inflection

‘Shōgun’ co-creators break down the finale: ‘It’s a story about death’

API startup Noname Security nears $500M deal to sell itself to Akamai

US think tank Heritage Foundation hit by cyberattack

NASA discovered bacteria that wouldn’t die. Now it’s boosting sunscreen.

How to watch ‘Argylle’: When and where is it streaming?

Tesla drops prices, Meta confirms Llama 3 release, and Apple allows emulators in the App Store

Tesla layoffs hit high performers, some departments slashed, sources say

TechCrunch Mobility: Cruise robotaxis return and Ford’s BlueCruise comes under scrutiny

Meta to close Threads in Turkey to comply with injunction prohibiting data-sharing with Instagram

Former top SpaceX exec Tom Ochinero sets up new VC firm, filings reveal

Consumer Financial Protection Bureau fines BloomTech for false claims

Thoma Bravo to take UK cybersecurity company Darktrace private in $5B deal

Summer Movie Preview: From ‘Alien’ and ‘Furiosa’ to ‘Deadpool and Wolverine’

Zomato’s quick commerce unit Blinkit eclipses core food business in value, says Goldman Sachs

Monsta X’s I.M on making music, gaming, and being called ‘zaddy’

Petlibro’s new smart refrigerated wet food feeder is what your cat deserves

The books on your favorite creators’ TBR shelf

Xaira, an AI drug discovery startup, launches with a massive $1B, says it’s ‘ready’ to start developing drugs

Rabbit R1 hands-on review: Something is iffy about this

UK probes Amazon and Microsoft over AI partnerships with Mistral, Anthropic, and Inflection

‘Shōgun’ co-creators break down the finale: ‘It’s a story about death’

-

Entertainment7 days ago

Entertainment7 days agoWhat Robert Durst did: Everything to know ahead of ‘The Jinx: Part 2’

-

Entertainment6 days ago

Entertainment6 days agoThis nova is on the verge of exploding. You could see it any day now.

-

Business6 days ago

Business6 days agoIndia’s election overshadowed by the rise of online misinformation

-

Business6 days ago

Business6 days agoThis camera trades pictures for AI poetry

-

Business7 days ago

Business7 days agoCesiumAstro claims former exec spilled trade secrets to upstart competitor AnySignal

-

Business5 days ago

Business5 days agoTikTok Shop expands its secondhand luxury fashion offering to the UK

-

Business6 days ago

Business6 days agoBoston Dynamics unveils a new robot, controversy over MKBHD, and layoffs at Tesla

-

Entertainment6 days ago

Entertainment6 days agoEarth will look wildly different in millions of years. Take a look.